【笔记】Option Greeks

基于格拉ECON5009课件的笔记;

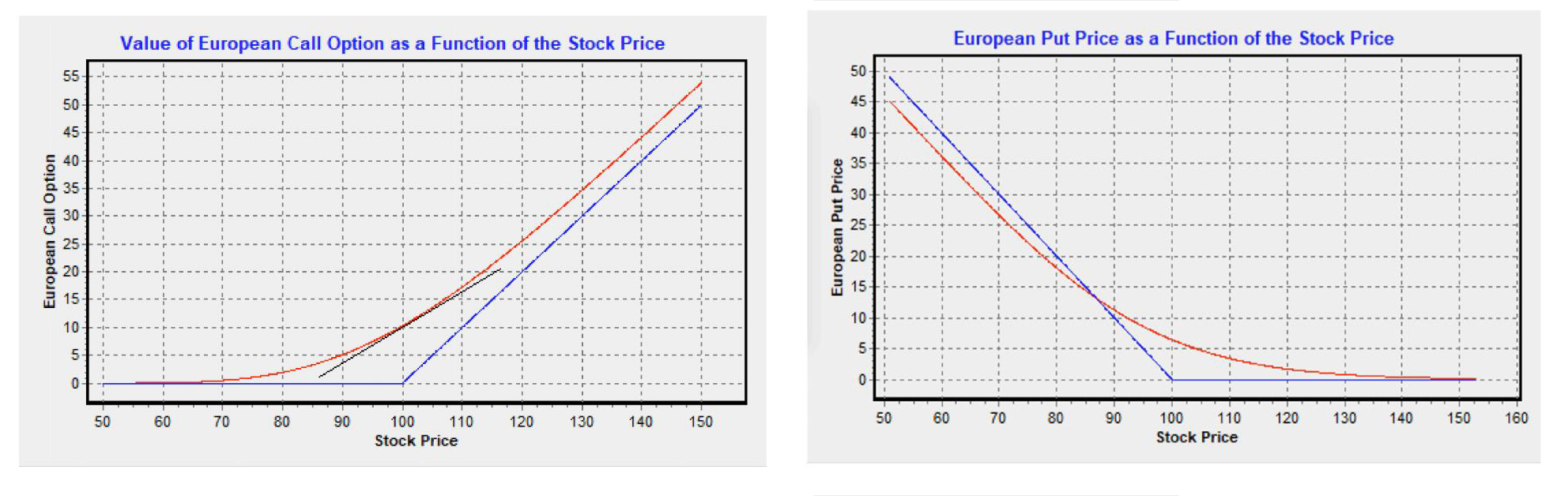

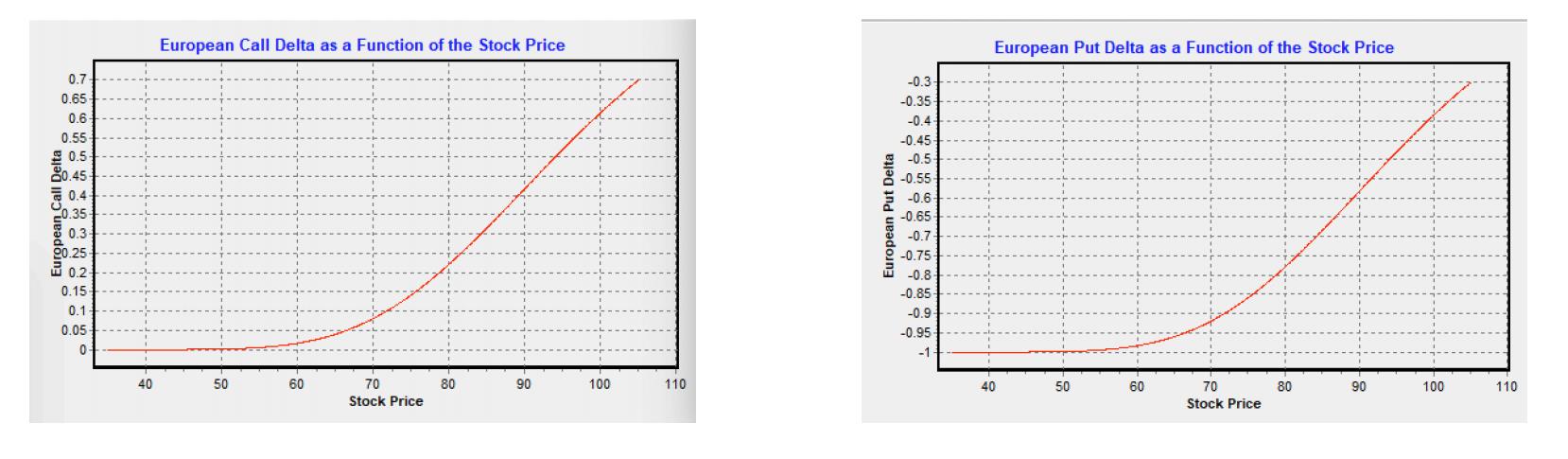

Without dividend

红线是在到期日之前的 Value,蓝线是到期日的 Intrinsic Value,差距是 Time Value

We have:

with:

and:

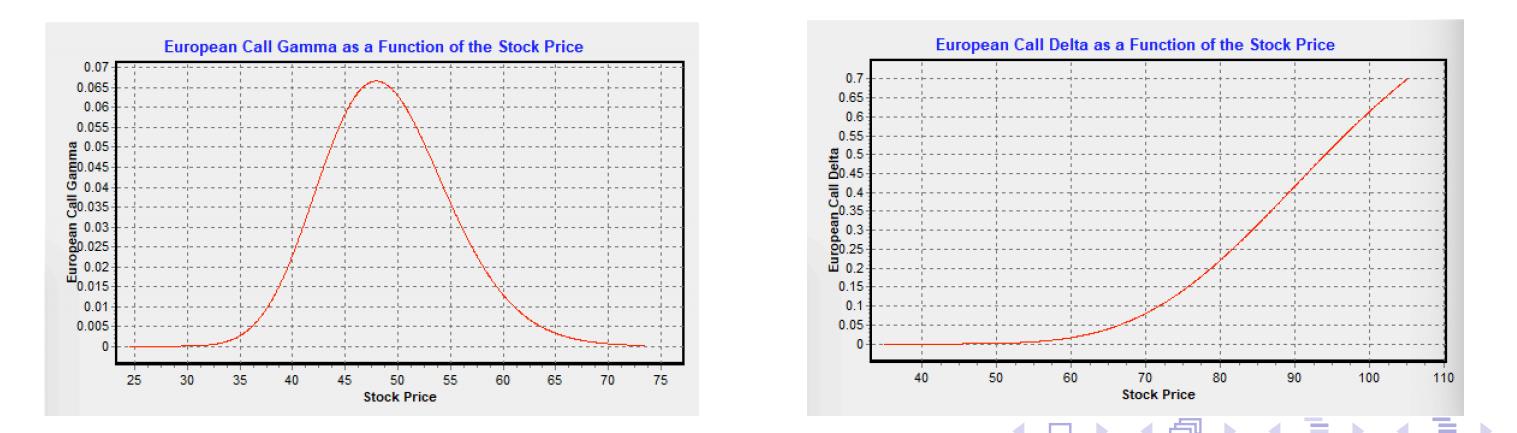

Delta

- Delta of a call is always positive(+); Delta of a put is always negative(-).

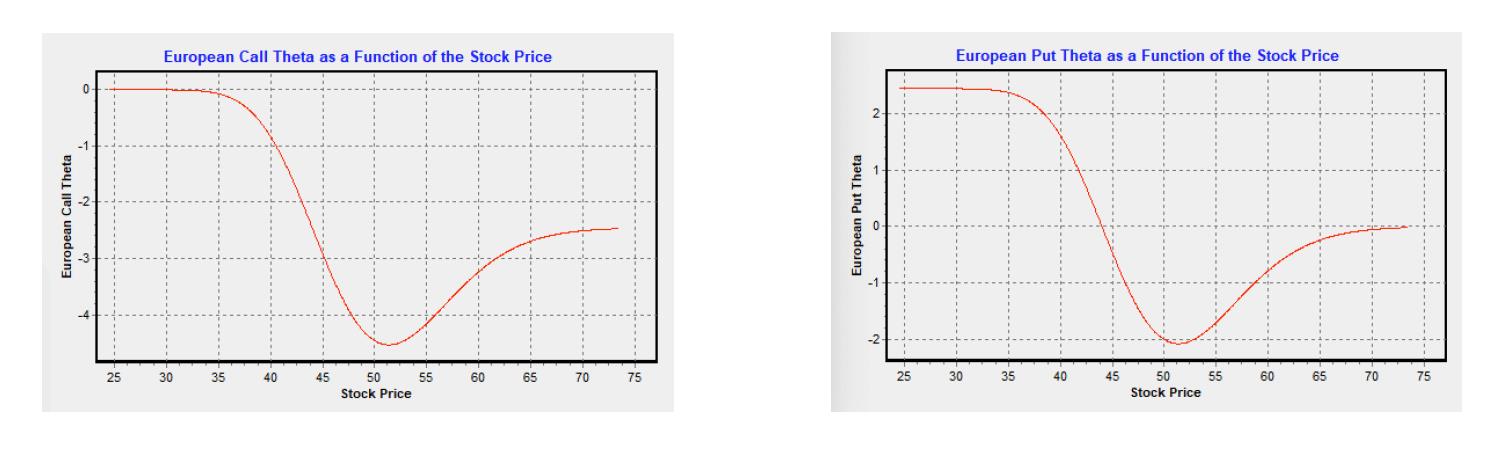

Gamma

Theta (When is measured in days, divided by 252)

With BSM PDE

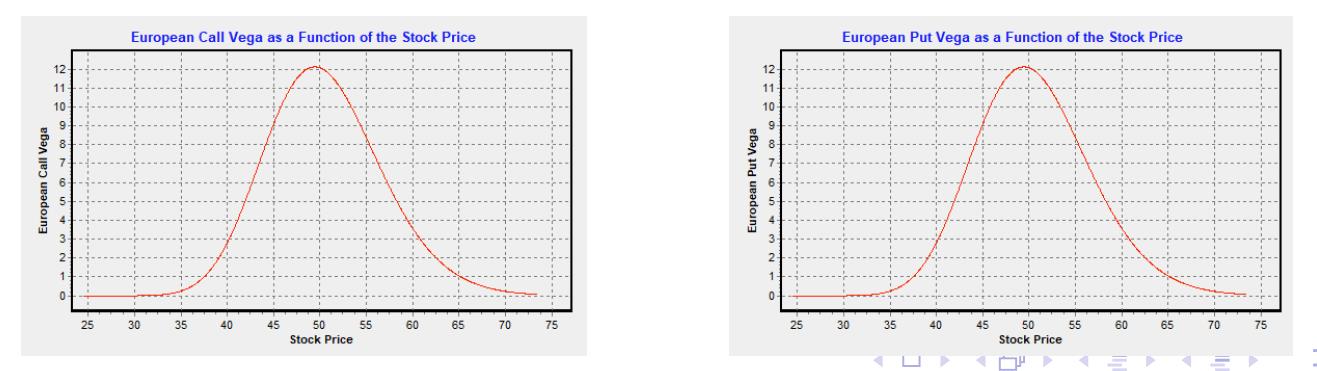

Vega

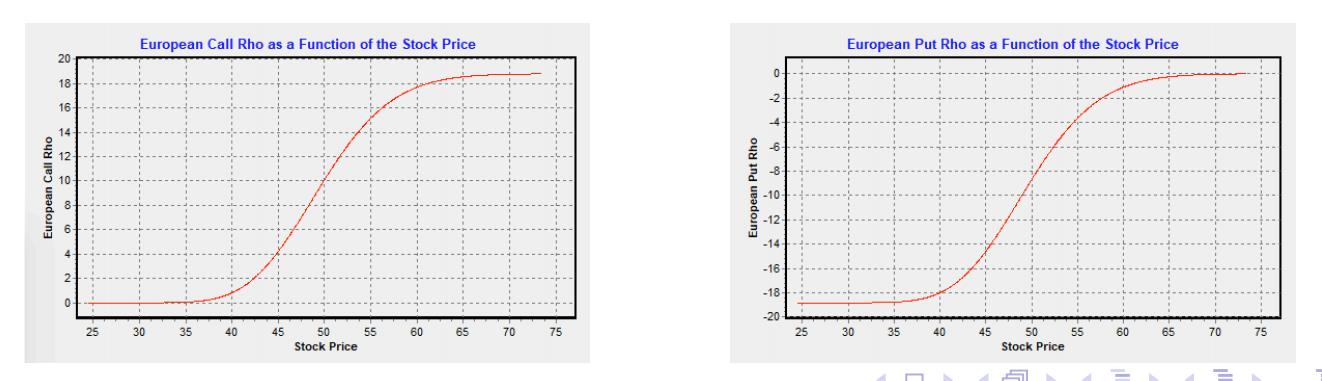

Rho

【笔记】Option Greeks

http://achlier.github.io/2021/03/05/Option_Greeks/